𝗧𝗵𝗲 𝗖𝗼𝗺𝗽𝗹𝗲𝘁𝗲 𝗣𝗿𝗲-𝗦𝗲𝗲𝗱 𝗙𝘂𝗻𝗱𝗿𝗮𝗶𝘀𝗶𝗻𝗴 𝗧𝗼𝗼𝗹𝗸𝗶𝘁

A full guide on how VCs evaluate pre-seed startups, a cap table calculator, a 600+ investor database, and 50 real pitch decks that raised over $380M

Hey! My name is Javier López, and I’m a Venture Capital investor at GoHub Ventures, an early-stage fund with €90M AUM investing from pre-seed to Series A internationally.

After reviewing 1,100+ startups this year, I wanted to share a detailed guide on how VCs actually evaluate your startup.

To make it more complete, I’ve teamed up with my friend Javier Martínez, who’s seen the game from both sides: from the investor’s perspective as an investment banker, corporate development manager, and advisor at GoHub, to now leading from the inside as the CFO of a Series A startup.

Together, we’ll be publishing a series of posts going stage by stage, explaining how investors evaluate companies at each phase, from the earliest pre-seed rounds all the way to private equity and even the M&A perspective.

We’ll also share a set of resources and tools we believe can help founders as they prepare for each round.

In today’s newsletter

We’ll focus on how early-stage VCs evaluate pre-seed startups, what they actually look for, and how they make investment decisions.

What’s inside

👉A detailed guide on the 8 key factors VCs consider when analysing a pre-seed startup

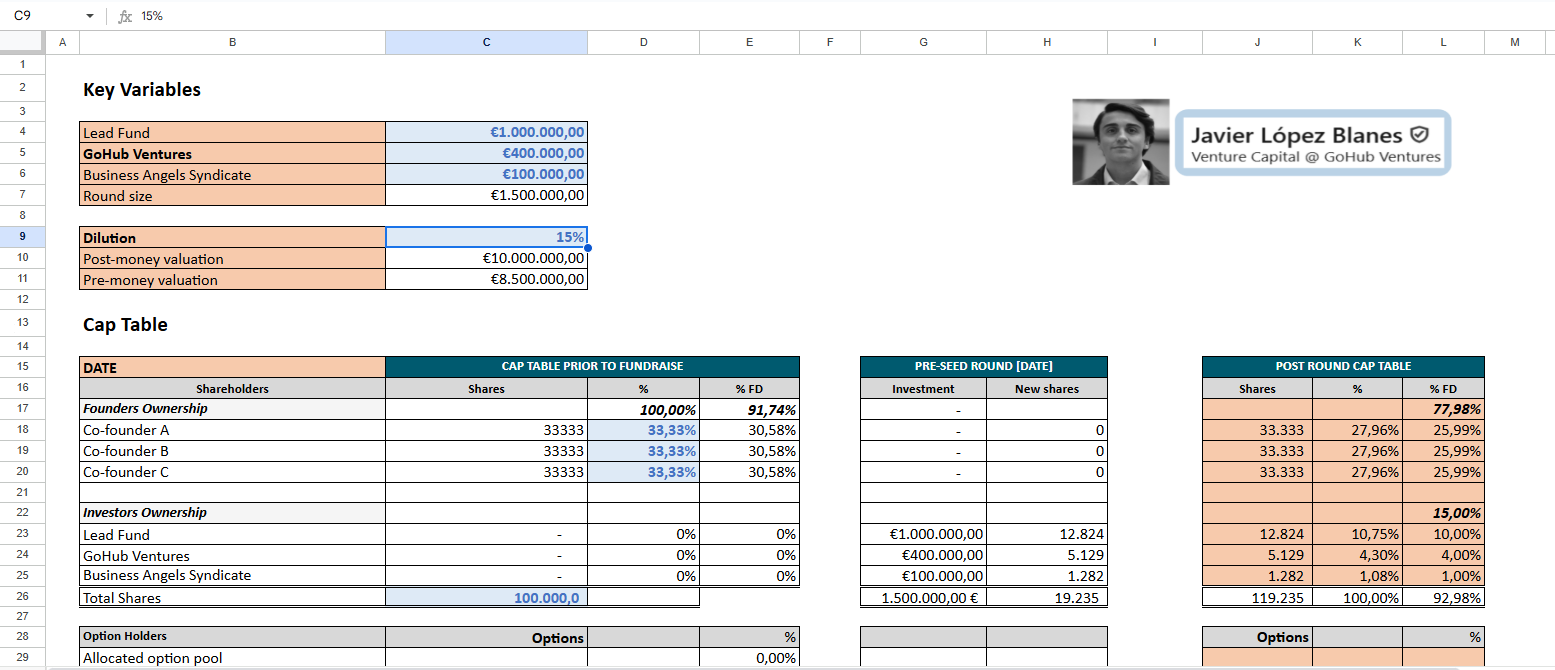

👉A cap table calculator that can help you decide how much to raise and how to structure your first round

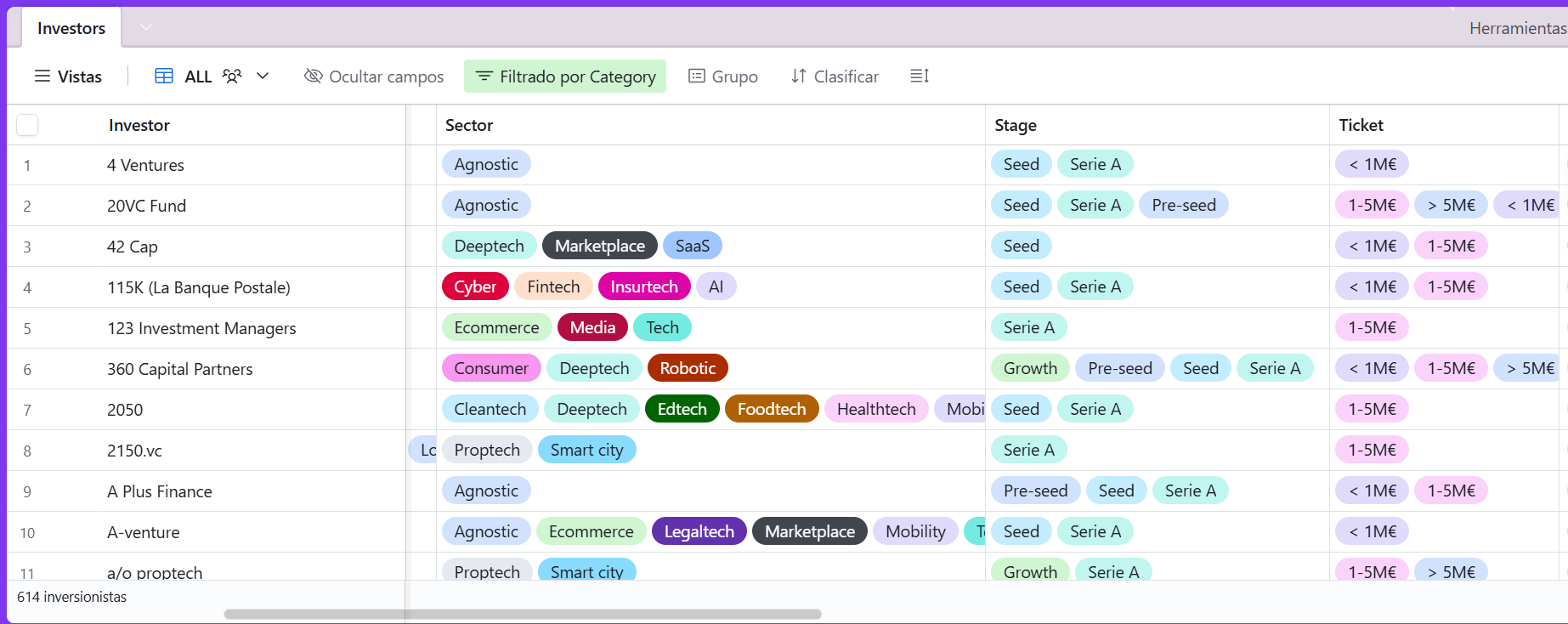

👉A database of 600+ investors with details on sectors, stages, geographies, and ticket sizes

👉50 real pitch decks from startups that collectively raised over $380M from pre-seed to Series A

This can be useful for:

Founders planning to raise their first round

Operators or aspiring investors who want to understand how early-stage funding works

Anyone curious about how VCs think when evaluating startups

Let’s get into it🚀

1. How VCs evaluate a pre-seed startup

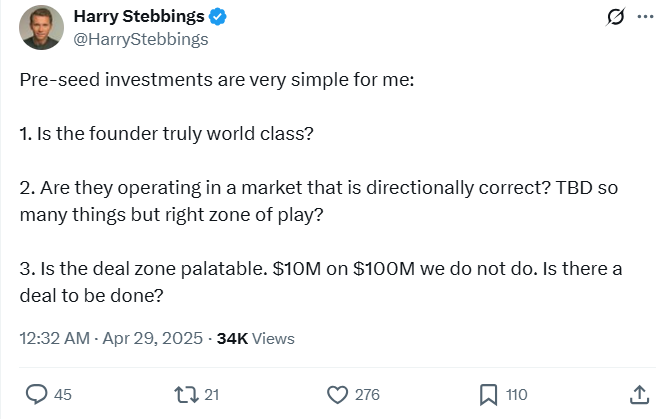

At pre-seed, VCs are basically trying to spot the top 0.5% of founders working on something in a big or fast-growing market and at a reasonable valuation.

I feel like this tweet from Harry Stebbings nails it perfectly:

1. Team

It all starts with the team. In fact, I’d say most VCs rank the quality of the founding team as the most important factor when deciding to invest in a pre-seed round. Markets shift, products will pivot and evolve, but great founders can adapt.

When evaluating a team, investors will look for proof of exceptionalism. Show them what you’ve done that sets you apart from your peers and why you’re the right person to build this company. Focus on aspects of your history that demonstrate hustle, tenacity, and efficacy.

VCs, like anyone else, rely on pattern recognition to judge what “world-class” looks like.

In my view, previous exits or past success as a founder are the strongest signals of all.

Other signals that tend to catch investors’ attention include:

Having held a key position or being an early employee at a well-known startup (e.g. ex-Stripe).

Deep domain knowledge is another strong signal, especially for niche products.

Having worked in selective environments like Big Tech, and even those not so tech-related like MBB or IB. The logic behind it is that these companies apply strict filters when hiring, so having been selected by them signals strong ability.

The same applies to top-tier universities.

You can even show exceptionalism through successful side projects, hackathon wins, or even achievements in competitive videogames or sports.

If you don’t have that kind of track record yet, don’t worry, there’s always a first time. But you’ll need to show your skill and sharpness in your meetings.

On team composition, YC usually recommends 2–4 founders, with at least 50% being technical if you’re building a tech startup (outsourcing your core tech too early is often seen as a red flag).

Investors also expect founders to be full-time and fully committed.

I also like to ask how the founding team came together, if you’ve known each other for a while or worked together before. It’s a good way to gauge team chemistry and how well you complement each other.

Vision is harder to measure, but after a few conversations, you can start to sense if a founder has the hunger, energy, and conviction to build a billion-dollar company.

2. Idea

Many investors often say they like founders solving personal problems, but I think that what they really mean is that founders should deeply understand the problem they’re solving: the pain points, the people involved, and how the process works.

In addition, it’s best to focus on daily or weekly problems rather than monthly or yearly ones, since it’s much easier to build something people use regularly than something they only need from time to time.

3. Market

On the market, VCs evaluate both the total size of the opportunity and the potential growth of the space itself. A company can have the best product in the world, but if the market isn’t large enough, it’s hard to get excited.

Moreover, we’ll try to understand whether it’s growing or declining (we try to spot signals of it, but no one really knows this for sure).

The best opportunities in this regard are those focused on spaces where billions are already being spent and/or where structural shifts can create new demand.

4. Product

The product by now might just be an idea, a prototype, or some early market feedback.

Having a working MVP at this stage is always a plus. However, many pre-seed startups successfully raise their rounds without one.

5. Traction

There’s usually no real traction (revenues) yet, other than conversations with potential customers or maybe early POCs. Founders can still show traction through a growing waitlist, early pre-sales, or a high conversion rate on a landing page.

You can also highlight customer testimonials, user feedback, or strategic partnerships, which help validate demand before revenue kicks in.

6. Timings

On timing, a typical pre-seed or seed round takes one to three months from first contact to close. Angels and micro VCs can move faster, while institutional investors tend to take longer.

Timing plays a role in how investors perceive momentum (and in generating FOMO). Good or bad, VCs are drawn to what feels “hot” so, when asked about your fundraising timeline, balance is key: saying “we’re closing this Friday” feels rushed, while “we’re closing sometime before 2026” feels cold.

The sweet spot is something like: “We’re grateful for the strong interest in this round. It’s important for us to choose the right partner, but things are moving fast.” It shows humility and momentum at the same time.

7. How much to raise and valuation

Finally, how much to raise and at what valuation to do so. YC’s advice on this one is simple: raise enough to reach profitability or, at least, your next fundable milestone.

The goal is to have enough runway to hit clear proof points without excessive dilution. For most pre-seed/seed rounds, that means raising for 12–18 months of operations.

Pre-Seed rounds usually range from $500k up to $2M.

Plus, at this stage, you don’t know what’s yet to come so maintaining ownership is key for optionality. Giving away more than 10–20% at pre-seed is often unnecessary and sets a bad precedent for future rounds.

As of Q2 2025, Carta data shows the median pre-seed valuation and round sizes across the 25th, 50th, and 75th percentiles in the US are:

Whatever amount you raise, make sure it’s tied to a credible plan. Have multiple versions based on different amounts raised, and clearly explain how each scenario changes your growth path.

8. Instrument

The majority of early-stage rounds under $4M are conducted on SAFEs or convertible notes, rather than priced equity. Additionally, according to Carta data, in Q2 2025, over 80% of SAFES had a post-money price cap.

One of the most common instruments for raising a pre-seed is the standard YC SAFE. It’s fast, simple, and founder-friendly, which is exactly what you need at this stage. Convertible notes can work too, but if you use one, I’d recommend keeping the valuation cap and discount (15–25%) within market norms.

Speed at this stage is everything. Founders should focus on keeping things moving forward and clean, while preserving optionality. Thus, I’d recommend avoiding boards, veto rights, or complex terms. Keep your structure simple for now so you can focus on building, not negotiating.

2. RESOURCES

👉 Cap Table Calculator

👉 Complete Investor Database

👉 50 Real Pitch Decks from startups that raised $380M+ across Pre-Seed to Series A stages

Sharing more stages soon, stay tuned!

| A guest post by

|